Overview

VWAP — the Volume-Weighted Average Price — is the average price of every share traded over a session, weighted by how much volume traded at each price. In one line, it answers: what did the “average share” actually change hands at today?

That makes it the single most important benchmark in institutional trading: the line big funds measure their own fills against, and a natural intraday dividing line between buyers and sellers in control.

Origins & history

- 1984VWAP was first used at the Wall Street firm Abel Noser, credited to Kyle Krehbiel — created not as a chart indicator but as a way to measure execution quality.1

- BenchmarkIt became ubiquitous because it is simple to compute and fairly reflects the day; “VWAP slippage” (your fill vs. VWAP) is still a standard measure of broker performance, and algorithms now route orders to beat it.1

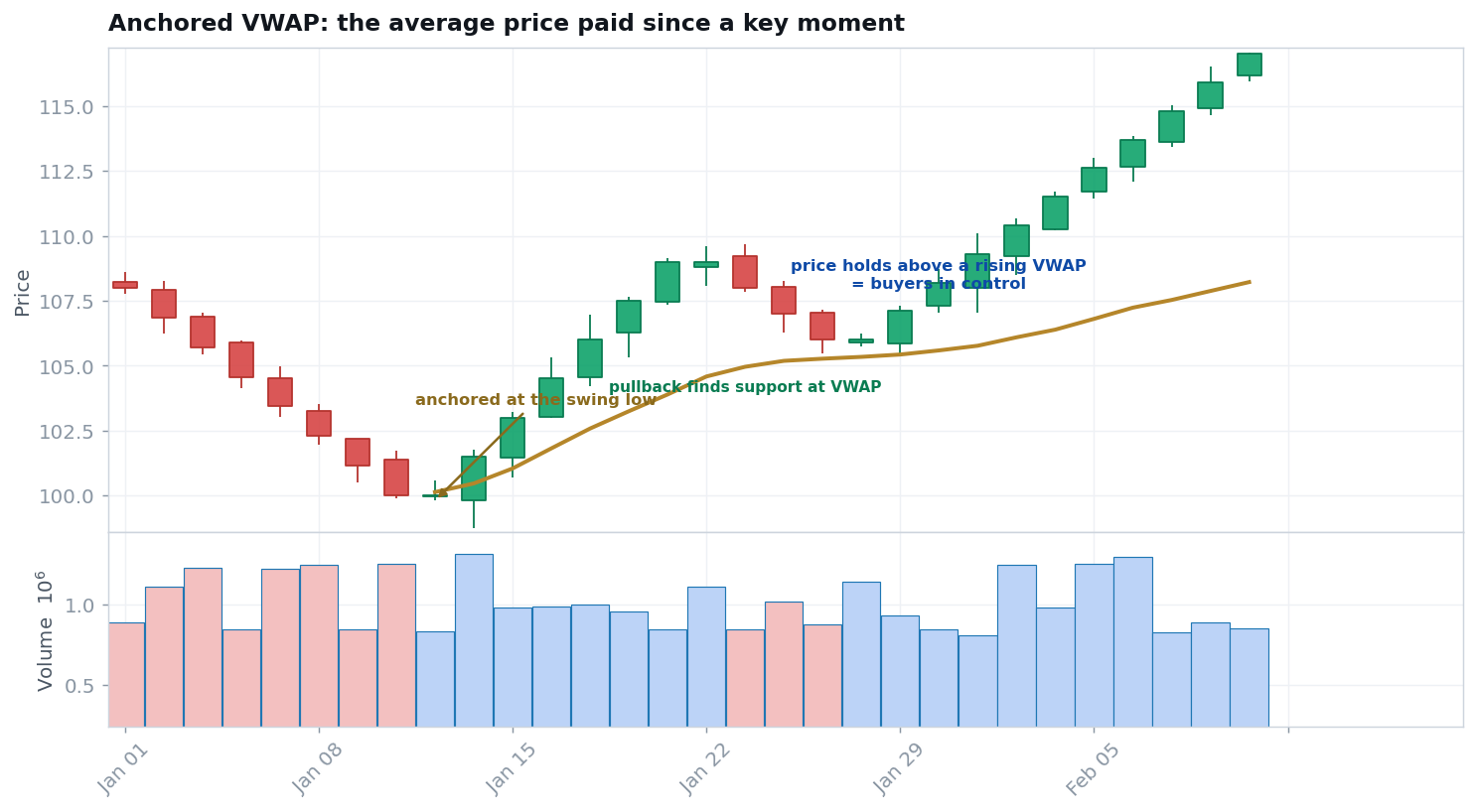

- ModernAnchored VWAP — measured from a chosen event rather than the day's open — was popularized for traders by Brian Shannon, who wrote the book on it.2

How it works

Because it is cumulative from the session's start and weighted by volume, VWAP is anchored to where real money actually traded — unlike a moving average, which is an unweighted rolling window. Standard-deviation bands are often added around it to mark stretched conditions. Anchored VWAP drops the daily reset and starts the calculation from a meaningful bar, extending the idea to multi-day swings.

Market psychology & mechanics

VWAP matters because so much capital is benchmarked to it. A fund told to “buy on VWAP” wants its average fill at or below the line, so VWAP becomes a magnet for institutional activity — buyers defend it, sellers lean on it. Above VWAP, the average buyer of the day is in profit and tends to support dips; below it, the reverse. It is less a prediction than a real-time read of who is winning the session.

Honest assessment

Strengths

An objective, widely-watched intraday fair-value line: excellent for execution, for reading intraday bias (above/below), and — in its anchored form — for finding meaningful support/resistance around events. Its institutional importance is what gives it teeth.

The evidence

It is essential to be honest here: VWAP was built as an execution benchmark, not a trading signal. There is strong industry use of VWAP for measuring and minimizing transaction costs, but little rigorous evidence that “buy at VWAP” is a standalone edge. Its value as a trading tool is as context — a level and a bias — not a system.1

Evidence rating: rock-solid as an execution benchmark; as a trading signal, useful for context only — no proven standalone edge.

Weaknesses & failure modes

- RESETIt resets daily. Standard VWAP is meaningless across sessions; for swing context you must use anchored VWAP.

- LAGIt's a cumulative average. Late in the day it barely moves, and it describes the past — it doesn't forecast.

- CROWDEDIt's heavily watched. Obvious VWAP reactions can be faded or gamed by larger players.

- CONTEXTNot a signal alone. A touch of VWAP is not a guaranteed bounce.

Professional uses vs. retail misuses

How professionals use it

- To benchmark and schedule executions (the original purpose).

- As an intraday bias line and a reclaim/reject level.

- Anchored from earnings or a major pivot for swing context.

Common retail misuses

- Buying every touch of VWAP as a guaranteed bounce.

- Using daily VWAP to make multi-day swing decisions.

- Treating it as predictive rather than as context.

How a modern prop trader uses it

Echoing the "context, not a signal" point above, prop trader Lance Breitstein treats anchored VWAP as a read of trend, not a level to trade off of. His working heuristic: don't short a stock holding above its anchored VWAP unless it has capitulated, and don't long one below it unless it has capitulated — a quick read of whether the average buyer since a key catalyst is in or out of the money, and how they're likely to behave. He anchors to fundamental or price events (an earnings gap, a breakout, a capitulation day) rather than the clock.

WATCH Lance Breitstein — "The Anchored VWAP Edge Most Traders Never Discover"

Going deeper

Variations: VWAP standard-deviation bands, moving VWAP (MVWAP), rolling/weekly VWAP, and anchored VWAP from any chosen event. Multi-timeframe: the daily VWAP frames the session; anchored VWAPs from a yearly low, an earnings gap, or a swing high frame the larger trend — alignment of several anchored VWAPs marks high-conviction levels.

Practice

Quiz 1 — How is VWAP different from a moving average?

VWAP is volume-weighted and cumulative from the session open (resetting daily); a moving average is an unweighted rolling window of the last N periods. VWAP says where money actually traded; an MA just smooths price.

Quiz 2 — Why does standard VWAP reset every day?

Because it's built as an intraday execution benchmark — the average fill price for that session. To carry meaning across days you use anchored VWAP from a chosen event.

Quiz 3 — Is “price tagged VWAP, so it will bounce” a reliable rule?

No. VWAP is context, not a signal. It marks a meaningful level and bias, but a touch alone is not a trade — you still need a setup and a stop.

This concept in the knowledge graph

Resources

- TRADERBrian Shannon — anchored VWAP.

- PLAYBOOKThe VWAP Scalp.

- GLOSSARYVWAP & anchored VWAP.